The word 'Retirement' brings a comforting thought to those who are working rigorously in their daily lives and are excited to spend a carefree life after 60. With life expectancy now touching 100 years, you have almost half of your life ahead to give time to yourself and relish it with comfort and ease.

Treat your investor's money as your retired father's money who has done his last savings and who is not able to earn again in life.

Read on to know how to plan for the retired life of your dreams. What lies ahead:

Can I maintain my current lifestyle when I retire?

The first step to planning for retirement is to find out how much money you should have when you retire. Our retirement calculator below can help with this:

What would be my expected monthly expenses

when I retire?

per month

*considering inflation at 4% and return rate at 11%

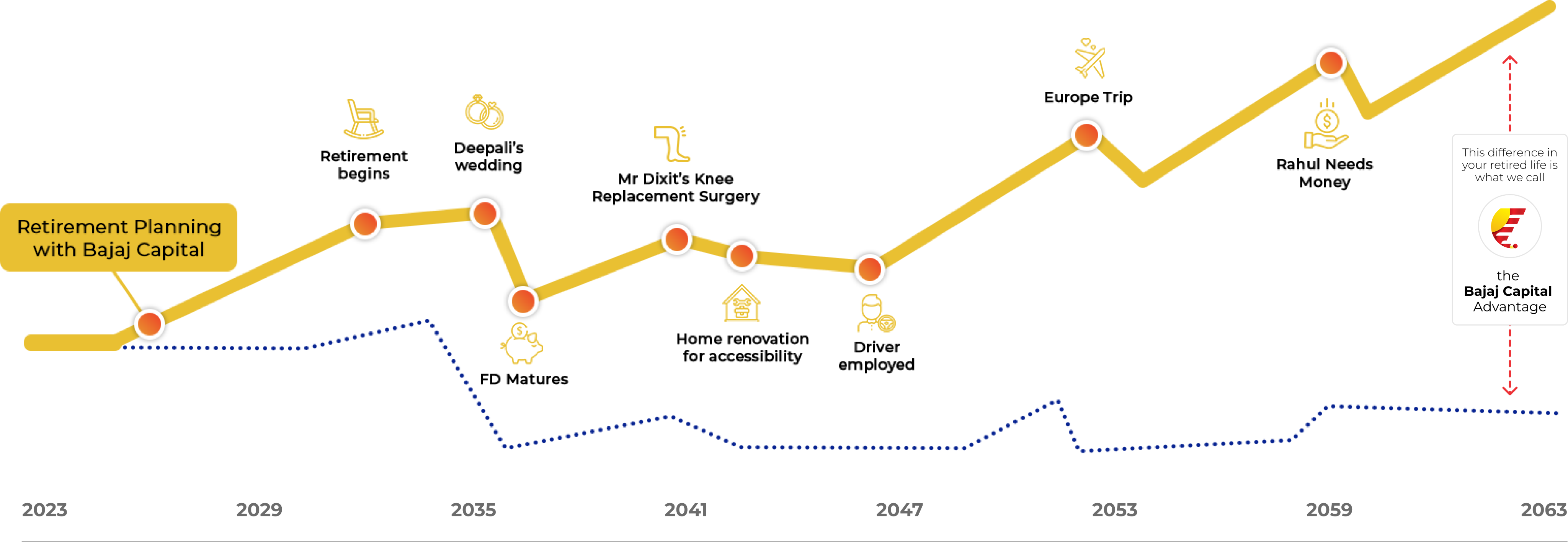

How We at BajajCapital See Your (Awesome) Retired Life

Map of a Retiree's Life | Mr Ravi Dixit & Mrs Abha Dixit

Mr Dixit is a 57 year-old salaried PSU employee nearing retirement. He lives with his wife Mrs Abha Dixit (53) who is a school teacher in Bhopal. They have 2 children - Deepali aged 27 and Rahul aged 32. Deepali is working in an MNC in Mumbai and Rahul lives with his wife and daughter in Bangalore.

Mr & Mrs Dixit's path

without the retirement plan.

Mr & Mrs Dixit's path

without the retirement plan.

Following Retirement Plan

recommended by BajajCapital

Following Retirement Plan

recommended by BajajCapital

Engaging with

BajajCapital Retirement Plan

Engaging with

BajajCapital Retirement Plan

- Mr & Mrs Dixit's path

without the retirement plan.

- Following Retirement Plan

recommended by Bajaj Capital

- Engaging with Bajaj Capital

Retirement Plan

Why You Can Trust Our Retirement Planning Engine

A judicious retirement plan is the best support one can have for a relaxed post-retirement life as it helps you plan and provide for the following:

A picture of your true future self

BajajCapital helps you visualise your true future retired self. Our intelligent retirement planning engine helps you save, invest and build an adequate corpus in your working years and then invest it diligently after retirement so that it provides you with the necessary cash flows to lead a financially relaxed post retirement life.

BCL ka bharosa

With 59+ Years of Experience delivering excellent financial decisions, you can rest assured that service by Bajaj Capital will be unparalleled.

Protection from falling interest rates on banks deposits

Interest rate on 3-year fixed deposit rates at SBI were 9.25% p.a. in Aug 2011. Today it is at 5.3%, a fall of 400 bps (or 44%) in 9 years Income of a person dependent on bank deposits would have almost halved in 9 years while expenses would be up more than 60%. Prudent retirement planning will help you mitigate such shocks to a great extent.

Protection from taxes

Taxes and Inflation are the two biggest enemies of a retiree. Most retirees look at gross income (before tax) while deciding on optimal investment option or strategy. However, improper tax planning can take away as much as 20-22% of your income. The good news is, you can reduce the tax liability using simple techniques and hence higher income in hand. A good Retirement Plan with us helps you do just that.

Counter Inflation

Rise in prices over the years, due to inflation, makes an enormous difference to the amount needed for leading a comfortable retired life. For instance, if you need ₹50,000 per month to meet your living expenses today, you will need ₹1,10,000 per month after 20 years and ₹2.4 lakhs (up by almost 5 times) per month after 40 years, at an annual inflation rate of 4%. With Bajaj Capital, your portfolio will be primed to provide for the rising expenses.

Medical Expenses

With rising age comes the need for preventive health checkups and several health problems that need the best of medical facilities. This can be expensive. Catering to these expenses can make a massive dent to your finances post-retirement.

Who should plan for Retirement?

Is Retirement Planning needed for all?

Everyone needs to plan for his/her

retirement. Non-salaried

people like professionals, actors and athletes need it more than anyone else.

Many people think that only salaried people need to plan for Retirement as they will not have enough funds once the regular source of income vanishes. As a matter of fact, salaried individuals who have mandatory Employee's Provident Fund (EPF) still have some corpus (though grossly inadequate) to rely on after retirement.

However, people who are not from the organized sector like businessmen, sportspersons, professionals like CAs, Lawyers and Doctors, who do not have such an option, need to plan well in time. This is particularly true for sportspersons, actors whose earning lives can be short and unpredictable. This means they have very less time for accumulating the required corpus and hence need Retirement Planning the most.

Common Myths

Myth #1

Retirement planning is done when one reaches a certain age.

In fact, retirement planning is deeply linked to surplus income and not age. The incidence of Retirement planning increases as incomes rise.

Myth #2

For retirement, one needs to plan only for major future expenses.

Most people fail to make adequate provision for contingencies like term insurance and rather worry only about expected (and positive) events like their children's needs (education, marriage etc.) This gap has been laid bare by the COVID-19 crisis, which has underlined the need to plan for income shocks, diversify sources of income and arrange for contingency funds and adequate medical and term insurance.

Myth #3

Parents can rely on their children for retirement needs.

In fact one out of four Indians say the fear of being dependent on family is a major trigger for retirement planning#. Earlier Indians tended to rely heavily on our children, likened to a reverse mortgage, promising to leave our wealth to children in return for care and financial support in old age. But as the young migrate and nuclear families proliferate, this contract is fraying. Indians are becoming more self-sufficient, seeking less financial dependence on their families after retirement.

Myth #4

One can feel confident about their retirement plan if all future financial needs are accounted for.

Unfortunately it's not that simple. Alarmingly, barely 1 in 5 Indians

consider inflation while

planning for retirement# - so having a plan alone is not

enough for financial

security. Even those who try to estimate a future monthly expenditure,

accounting for inflation,

may find their calculations upended by unexpectedly large expenses and

even medical inflation -

which can be much greater than overall inflation.

Similarly, only a

handful of Indians

actually cover for other critical external events like economic

slowdown, stock market

volatility or instability in government regulations or interest rates.

The flipside is that despite all this, Indians are also increasingly anxious about their future and ready to take positive action.

#As per PGIM India Mutual Fund Retirement Readiness

Survey 2020

Phases in Retirement Planning

Calculate the Retirement Corpus needed

The quality of your post retirement life depends on your ability to correctly estimate the retirement corpus needed at the time of your retirement. While computing the adequate amount of retirement corpus needed, it is always better to be conservative.

The following factors need to be considered while estimating your retirement corpus -

- The corpus must last your lifetime and more. Average human lifespan has increased. Plus there is a good chance that your spouse may outlast you. Plan up to age 100 (of the younger partner) at least.

- Be conservation while estimating monthly expenses required after retirement. Adjusted them for inflation.

- The expected returns on the corpus, adjusted for the declining trend in interest rates.

- The amount your wish to leave for philanthropy or as gift/ legacy for your future generations.

- Provide for lumpsum outflows for emergency medical care, children's marriage, etc.

- The retirement corpus should not be mixed with other goals

Inflation and falling interest rates are the biggest enemies of a retiree.

Let us see how each of these 2 factors impact your required retirement corpus.

Inflation

Inflation diminishes a Retiree's buying power. Even if overall inflation remains low, some components such as Healthcare tend to grow at a much higher rate (also known as medical or healthcare inflation). Your expenses on healthcare tend to go higher (as a proportion of your total expenses) as you age.

See how inflation increases your expense budget over time:

Rate of Inflation

₹50,000

₹74,012

₹1,09,556

₹1,62,170

₹2,40,051

At inflation of 4% p.a. your monthly expenses double in 20 years, more than triple after 30 years and multiply by 5 times after 40 years.

Imagine you target a retirement corpus of ₹1 crore assuming monthly expenses at ₹50,000 today and by the time you retire in 30 years, you find you actually need ₹3 crores as expenses have tripled!

Falling Interest Rates

Long Term Trend in Bank Deposit rates shows they are in a secular decline after having peaked in FY 1995-96 at around 12%. The decline lasted till FY 2003-04 after which they rose to more than 9% in FY 2011-12. They are falling again since then and are at around 5% levels today, a fall of ~400 bps or 44% from the FY 2011-12 peak. Interest rates on 3-year fixed deposit rates at SBI were 9.25% p.a. in Aug 2011. Today it is at 5.3%, a fall of 4% in 9 years. A monthly interest income of ₹50,000 per month in 2011 would be just ₹28,700, if you renew the deposit today. Your monthly expenses would have gone up from ₹50,000 to ₹81,000 in the same period as per the Income Tax Department's Cost Inflation Index. If interest rates can fall by this much in such a short period of time, imagine how low they can go in the next 30 years. Prudent retirement planning can help you mitigate such shocks to a great extent.

Saving and Investing to build your retirement nest

The amount you accumulate as retirement corpus is determined by the simple equation -

Amount = P*(l+r)n

Where -

- Pis the principal invested

- ris the rate of return on the investment, and,

- nis the time-period for which one is invested

In this, the time-period (n) has an exponential (biggest) impact on your final amount. A small increase in it can lead to multifold growth in your portfolio value.

Next comes ‘r’ or rate of return on the investment. The principal invested has the least impact on the final portfolio value.

Start early, give more time to your investment to benefit from compounding.

| Late by 5 years | Late by 10 years | ||

|---|---|---|---|

| Scenario | A | B | C |

| SIP amount | 10000 | 17000 | 29000 |

| Tenure | 30 | 25 | 20 |

| CAGR | 10% | 10% | 10% |

| Annual SIP Growth Rate | 0% | 0% | 0% |

| Principal Invested | 36,00,000 | 51,00,000 | 69,60,000 |

| Corpus | 2,06,28,433 | 2,09,66,523 | 7,47,09,237 |

If you start late you have to invest a disproportionately higher amount to get the same corpus on retirement.

A delay of 5 years means your monthly SIP amount has to go up by 70% to get the same corpus.

A delay of 10 years means the SIP amount has to be 3 times of the

original amount, in order

to get the same corpus.

The bigger the time span you give

the Retirement Plan to grow,

the bigger the Retirement Corpus becomes.

Work towards owning your home

Owning a home is a necessity and a dream. And that's not it. Your home is that asset that provides you with several other benefits: a sense of security, additional rental income, capital gains in the medium to long term, etc. Moreover, savers who buy tangible assets for investment, value their tangible goods as a form of value diversification and a hedge against any economic uncertainty. For a retiree, there is nothing more comforting and assuring than having his/her own home to live.

Real Estate as an asset class has a low positive correlation with stock and bond markets. Investment in real estate, such as owning your home, can provide you benefits such as rental income, reverse mortgage, etc. Simultaneously, these reduce your exposure to overall market risk in a manner that most intangible are incapable of doing.

It is better to buy your home using a home loan rather than waiting to accumulate the requisite amount. It gives significant income tax benefits – both on interest paid and principal repaid. However, one must try and clear the loan at the earliest. Never retire with an outstanding loan on you.

Income Tax benefits - use them to your advantage

Money Saved is Money Earned! We can say this very well for the tax saved on our investments, which can be further invested to produce more money. And this feature has to be on-board along with you in your Pre as well as Post - Retirement journey as well. Your investments for retirement can be invested in instruments that help you save tax.

There are 2 kinds of tax efficient instruments – 1. Instruments that are eligible for deduction (generally u/s. 80C) when invested in (PPF, ELSS, NPS, ULIPs, etc), and, 2. Instruments whose maturity or redemption proceeds are exempt from tax (PPF, NPS, ULIPs, etc). As you can see, instruments like PPF, NPS and ULIPs carry both the benefits, while gains on redemption from ELSS funds are taxable as long term capital gains.

For instance, let us take the case of Tax Saving Equity Linked Savings Schemes (ELSS) schemes of Mutual Funds. They have a well-diversified equity portfolio like any multi cap equity fund. However, as an added benefit, investments in ELSS funds are eligible for deduction u/s 80C. This means, for every ₹1,00,000 invested in ELSS, the investor (assuming she is in the 30% tax bracket) saves ₹31,200 in taxes. This money, which would have been paid in taxes otherwise, can be saved and invested. As a result of this, one’s investible surplus goes up by 31.2%, which if invested diligently, can lead to a much larger corpus at the time of retirement. This is also true for investments in PPF (Public Provident Fund), NPS (National Pension System) and ULIPs (Unit Linked Insurance Plans), both of which enjoy significant tax benefits leaving extra investible surplus in the investor’s hands.

All these instruments are excellent tools for wealth creation for long term goals and should be used judiciously after due diligence in consultation with your investment advisor.

Protect yourself and your family - Insure your Health, Life & Key Assets

Inflation is soaring, but the cost of private health care is rising even faster. As per an industry estimate, health-care costs in India are rising by 13 to 14% every year. The only way one can safeguard finances against the rising medical bills is by buying a Health Insurance Policy. Other than that, one needs to safeguard the future of his/her loved ones with a Life Insurance cover and have the needed tangible assets such as one's own home to give them a sense of security they need.

Health Insurance - Health Insurance is your safety net for your finances in the event of any expensive health care requirement or any medical exigency. Health Insurance plans offer variants such as individual insurance and family floater. An Individual Health Insurance plan is separate insurance for an Individual with the defined cover, whereas a Family floater plan covers an entire family, and the coverage can be used by any member of the family individually.

Life Insurance - When one considers the possibility of investing in life insurance, one of the first questions that one faces is – who should buy life insurance? The answer to this lies in the financial situation of the investor. Generally, anybody who has a financial dependent would benefit from investing in life insurance. Financial dependents could be your children, your spouse, a sibling, or even your dependent parents.

Another set of people who should buy life insurance are investors who want to enjoy tax savings benefits along with long-term capital appreciation. A life insurance policy is amongst the few investment options which offer both of these advantages. Other than these advantages, there are many other ways in which life insurance can help the investor.

Getting a Life Insurance cover is amongst the most important steps one takes for securing his / her family's future. It also provides several tax-saving benefits along with long-term capital appreciation.

How does BajajCapital help me in Retirement Planning?

BajajCapital is an industry stalwart in the Financial advisory domain for over 5 decades and has been helping people secure their financial tomorrow. Since our inception in 1964, we have been ensuring that each of our clients knows the right way to make use of their financial resources and land to their desired future. With our arms spread through more than 200 offices in 100 cities, we are a household name in India for producing a bright future.

We know you, We understand you

Knowing you and Understanding you is the most critical part of retirement planning. Every person has a unique set of needs, risk appetite, return preferences and liquidity requirements. One solution can never suit all.

Our state-of-the-art Risk Profiler helps us understand you better and provide the most suitable solution. This helps us ensure that Retirement is the best and most cherished part of your life. The Retirement corpus is then invested in the right avenues that meet the accepted risk, return and liquidity criteria and provide adequate cash flow to meet all ends.

Focus on Total Well-being

Total wellbeing takes into consideration the physical; social/emotional; financial; community; and environment. Each component alone can have a direct impact on you. All areas of personal wellbeing get a boost when financial wellbeing improves, as all elements of an individual's wellbeing are interconnected

When it comes to Retirement, small day-to-day decisions about finances, including how one thinks about the purpose of money, can make a big difference in overall health and wellness, leading to greater opportunities and a better time. At the individual level, a workplace filled with proper balance will certainly gain tremendous value from supporting financial education and voluntary benefits, which are valuable for overall benefits

Flexibility

One of the most challenging aspects of creating a comprehensive retirement plan is striking a balance between realistic return expectations and a desired standard of living. The best solution is to focus on creating a flexible portfolio that can be updated regularly to reflect changing market conditions and retirement objectives.

We at Bajaj Capital have do Retirement planning with thinking about your retirement goals and how long you have to meet them. Then we ask you to look at the types of retirement accounts that can help you raise the money to fund your future. As you save that money, you have to invest it to enable it to grow.

Last Mile, Research-backed, Actionable Advice

A lot of individuals/ retirees end up investing on their own, but when it comes to retirement savings it’s a good idea to work with a financial advisor who has a certified financial planning designation. 4 things we ensure to look for when creating and giving you a Last Mile, Research Backed Actionable advice

1. Qualifications: CFP is the most widely recognized financial advisor designation.We ensure that your plan is made and continuously monitored by a CFP so that you are always assured

2. Services they provide: Our team specialize in retirement planning, We help you create a budget and also sell right securities.

3. Track record: Ask to speak to references. Our advisors are attentive, understand your needs, can create solid plans and know how to help you invest. We are in the business since 1964, and have taken pride in managing Wealth for 3 generations

4. Communication: There may be time when you may tend to panic when the markets get bad and when their advisor doesn’t’ reach out to tell them to stay calm. Our digital processes ensure that the advisor wants to meet you and also lets you be in touch with them. You may not need handholding, beautiful you do want to meet with they are always ready and we ensure that our expert connects with you at least a couple of times a year.

Our approach

We provide customized solutions, devised using a scientific retirement planning tool developed after deep analysis & research. This tool produces a Retirement Plan with multiple benefits. It follows the SLR principle of Safety, Liquidity and Returns, in order of importance.

-

LIFETIME CASH FLOW PLANNING

The tool provides a scientific mechanism to plan your investments in a holistic manner and gives you a smooth Cash Flow Plan for a lifetime. You can literally see the monthly cash book for the next 40-50 years of your life in a single graph and table, with the source of inflows and outflows being clearly mentioned. It is like seeing the next 40-50 years of your life playing out in front of you on a screen.

-

POST TAX RETURNS

The scientific tool endeavors to optimize the investments and strategies in a manner that the cash flows are adequate to meet your needs on a POST-TAX basis. Taxes no longer come as a surprise to you.

-

LIQUIDITY

While the tool ensures that solutions are customized as per your needs, it also maintains enough liquidity at all times. At any point in time throughout your retired life, at least 60% of your portfolio can be liquidated at a couple of days’ notice.

-

MAX PORTION OF PORTFOLIO IN GUARANTEED SCHEMES

The Retirement plan ensures the safety of Capital and Returns by suggesting material allocation to instruments that enjoy sovereign guarantee and/or help you lock-in returns for long periods of time (works very well in a scenario where interest rates are expected to decline in the long run).

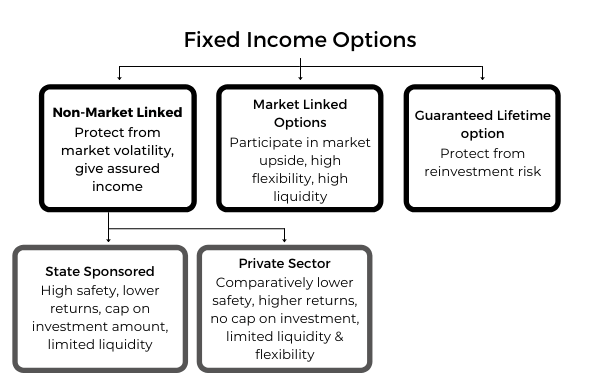

Diversified Multi-Asset Portfolios providing a combination of Safety, Income & Growth for your retirement needs

A customized and diversified Multi-Asset portfolio of the most suitable investment options is created to give you a combination of Safety, Income & Growth. The right blend includes:

-

Top Government Schemes

We give you the right mix of Government/ PSU sponsored instruments to ensure your Capital's safety

-

Best of Private Fixed Income Instruments

The best of the private fixed income instruments are selected to ensure the stability of returns allowing adequate cash flows.

-

The Right Exposure to Mutual Funds

Your corpus gets the right amount of equity exposure through specialized structures that ensure participation in upside while containing the downside in equity markets. The limited equity exposure ensures that your corpus is growing as expected to counter the effect of Inflation and increased living expenses. Additionally, most tax-efficient instruments are chosen for the portfolio to give you maximum benefit.